As a resident of South Florida, I’ve witnessed firsthand for years the impact of climate change and sea level rise on people and property. Most coastal communities here are already experiencing beach erosion and pockets of street and property flooding that are only getting worse as sea level rises.

In addition to beach erosion and sea level rise flooding, many cities and towns throughout Florida have also been hit by hurricanes supercharged by global warming that have caused tens of billions of dollars in damages. Here, too, sea level rise plays a role as higher seas mean stronger and more damaging storm surges.

Hurricane Ian is the latest super-charged storm to bring death and destruction to the Sunshine State. Sadly, more than 100 lives were lost to the storm in Southwest Florida. And the latest estimates are that it will take $75-100 billion to rebuild the homes, businesses and infrastructure destroyed by the mega-storm.

In addition to destroying many lives and billions of dollars in property, Hurricane Ian also rolled over Florida’s already wrecked property insurance market. Before the storm, fraud — mainly involving roofers replacing roofs before its necessary and billing insurance companies for the work — and costly storms created a marketplace where Floridians pay three times the national average for homeowners insurance. The losses have been so bad that many insurers have already fled the state or gone out of business, leaving Citizens Insurance, the state-run insurer of last resort for homeowners who can’t get policies elsewhere, to pick up the slack. Citizens now has more than one million policies, and there’s no sign the explosive growth will slow anytime soon. If anything, Hurricane Ian is going to force more private insurers out of business forcing tens of thousands more homeowners onto Citizens’ rolls.

Further complicating the insurance problem is the fact that only around 20% of Floridian homeowners carry flood insurance because they can’t afford it or they underestimate the threat. This is especially tragic considering that Hurricane Ian caused serious flood damage not only to coastal communities but well inland in counties where people never guessed they’d get hit by high water.

Earlier this year, the Florida state legislature held a special session to consider ways to alleviate the high cost of homeowners insurance but left without anything to show for the effort. The questions at this point are: 1. Why doesn’t anyone know what to do to fix Florida’s insurance problem? and 2. Is it possible that there isn’t any way to address it?

The first question needs to be posed to political leaders, insurers, and business and consumer groups. Together, perhaps, they can figure out how to crack down on roof repair fraud and find a mechanism to subsidize the cost of insurance for owners who can’t afford it.

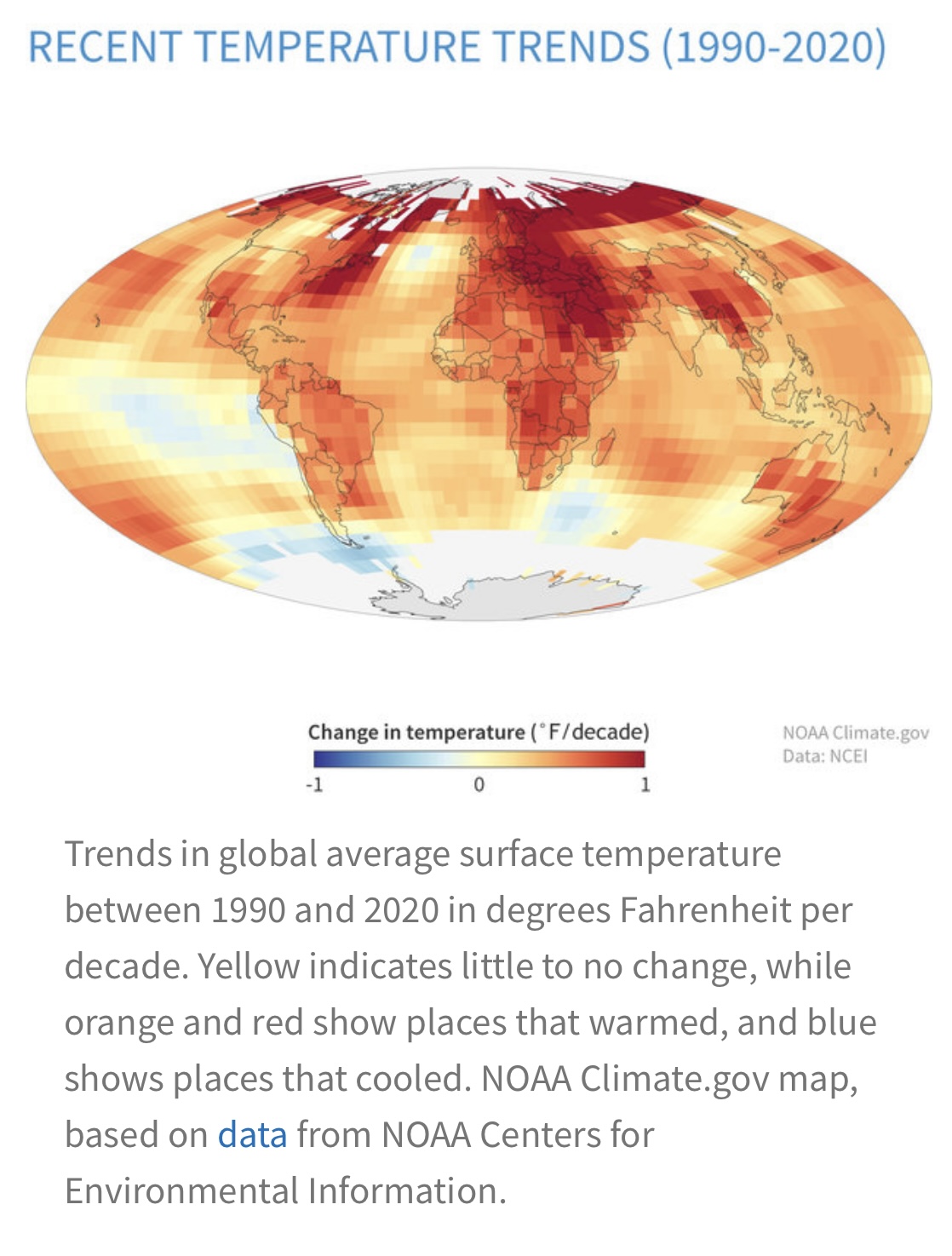

The second question may make the first question moot. It’s clear that climate change and sea level rise are going to get worse for decades to come. This is mainly due to the fact that humans aren’t reducing the amount of fossil fuels — oil, coal and natural gas — we burn, which is releasing record amounts of greenhouse gases into the atmosphere. Basic science says more carbon dioxide and methane mean more global warming, sea level rise and ever more powerful hurricanes, tropical storms and downpours.

The end result is that even if fraud is eliminated as a problem for Florida insurers, sea level rise flooding, mega-charged hurricanes with damaging storm surge that reaches further inland, and flooding from rainstorms are going to continue to increase as a challenge to coastal communities. As Hurricane Ian proved, even communities well inland can be hit by devastating floods from heavy rains.

If that’s not enough, sea level rise is pushing ocean water inland underground in areas that have porous limestone, sand, and even lava, as its foundation rock, which pushes the freshwater table up toward the surface where it has the potential to promote flooding well inland. This scenario is already being realized in some neighborhoods in South Florida and Hawaii.

The ultimate danger of a collapse of the home insurance market is not only that owners won’t be covered for their losses but mortgage providers won’t want to share the risk on uninsured properties and they will no longer provide loans. This will lock up a real estate market and cause a collapse in market value.

In Florida, homeowners of modest means are already going without insurance because the cost is too high. And some are considering selling their properties here because they can’t afford the carrying costs.

Florida is seriously at the front line of the climate change and sea level rise battle. Homeowners in other states watching what happens in the insurance market here should pay heed. The Sunshine State experience is likely portends their future and it’s anything but bright.

You must be logged in to post a comment.